It has been decades since banks started relying on legacy systems. These were engineered for stability and not speed. These platforms were created to help banks complete their daily routine work. It was powered for growth, ensured reliability, and supported regular compliance requirements that were applicable at the time.

However, today, we are a part of a fast-paced world. The same systems are limiting agility, constraining innovation, and inflicting risk. Something that was considered a technical debt has now turned into a strategic leadership challenge.

So, legacy modernization in the banking sector is no longer just an IT initiative. It is becoming a defining leadership strategy that directly impacts trust, resilience, long-term competitiveness, and regulatory confidence.

Traditionally, the banking leadership was associated with governance, financial discipline, and risk control. Even when these priorities remain the same, the definition of an effective relationship has certainly expanded. Now, leaders are expected to ensure uninterrupted digital services, respond rapidly to changes in regulatory guidelines, protect data integrity, and compete with the agile fintechs. Everything needs to be done simultaneously.

Legacy systems are at the centre of this challenge. The systems have an ageing architecture, monolithic code, tightly coupled applications that increase operational fragility and slows down decision-making. Leaders are therefore being judged not by the way systems are run, but by how they can evolve with the growing ecosystem.

Therefore, legacy modernization in banking is a leadership mandate. It is something that determines whether the institute has adapted without disrupting regulators and customers.

Modernization decisions now appear routinely on the boardroom and executive agenda. The reason is that the impact is far beyond technology. Banking system modernization has a clear impact on brand trust, enterprise risk, growth strategy, and compliance posture.

The system of banks processes millions of transactions on a daily basis, enforces business rules and regulations, and underpins reporting. In case of any failure, it can trigger financial penalties, regulatory repercussions, and massive reputational damage. Therefore, core banking modernization is no longer delegated only to the IT department, but needs executive sponsorship, long-term vision, and cross-functional governance.

Leadership has now started recognizing the legacy platforms which might limit the ability of a bank to do the following.

In this scenario, modernization is not only about getting rid of the old system for the sake of technology, but it is also about protecting the future of the institution.

Regulators are constantly expecting real-time reporting, transparency in data lineage and complete audit trails. Legacy platforms are often reliant on batch processing and fragmented data stores, which are unable to meet these expectations properly.

Modern architecture ensures regulatory compliance is enforced easily and demonstrated. They support automated reporting, standardized control, and consistent data governance, which reduces both regulatory risk and compliance effort.

Over time, the legacy environment keeps accumulating manual processes, custom integration, and undocumented dependencies. These can create hidden points of failure, which show up during audits, system changes, and peak load time.

In such an environment, modernization is the only choice as it becomes a form of proactive risk mitigation. As it reduces technical complexity, simplifies architecture, and improves observability, leaders can reduce operational risk rather than react to incidents.

Several banks still rely on mainframes for mission critical workloads. Undeniably, the mainframe is still powerful. The challenge lies in the age of codebases and the shrinking pool of specialized talent.

Strategic mainframe mitigation executed incrementally rather than abrupt replacement will help banks modernize capabilities and preserve stability. Leadership involvement is critical to ensure that migration is governed, aligned, and paced with business priorities.

Customers will no longer tolerate outages, even when they are for maintenance. Digital banking has become widespread and is expected to be available around the clock across different geographies and channels. In case of any interruptions, it will lead to immediate dissatisfaction and long-term loss of trust.

Therefore, banks need to prioritize zero downtime during modernization. It should be a result of deliberate strategy, leadership commitment to resilience, and planned execution.

Today, fintechs operate on cloud-native, modular platforms that enable rapid experimentation and deployment. Traditional banks remain constrained by Legacy core systems and struggle to keep pace with the growing space.

Modernization will help them compete while retaining the trust, regulatory compliance, and scale that FinTech often lacks.

Leading banks mostly avoid large-scale replacements, which can lead to unacceptable risks. Rather, they mostly adopt incremental approaches, which can result in gradual modernization of functionality while maintaining the core service running.

The method will help business units to see value immediately, align modernization with operations, and reduce disruption.

Introducing API layers and other integration platforms can help banks separate customer-facing innovation from core transaction processing. It will help to make faster development cycles while protecting the stability of the system.

These strategic approaches are foundational to an effective banking system and modernization. It will help modern and legacy platforms to coexist during transformation.

Running old and new systems in parallel will help teams validate performance, data, accuracy, and reliability before fully cutting over. The approach is highly beneficial for reducing migration risk and supporting a zero-downtime transition.

Leadership oversight is extremely important in this case, as it helps balance speed with assurance and ensure informed go/no-go decisions.

The success of modernization depends on preserving traditional accuracy and historical data. Automated reconciliation, advanced monitoring, and observability ensure that issues are detected early, before they escalate.

These are essential capabilities, not only for operation but also for sustaining regulatory compliance throughout the transformation.

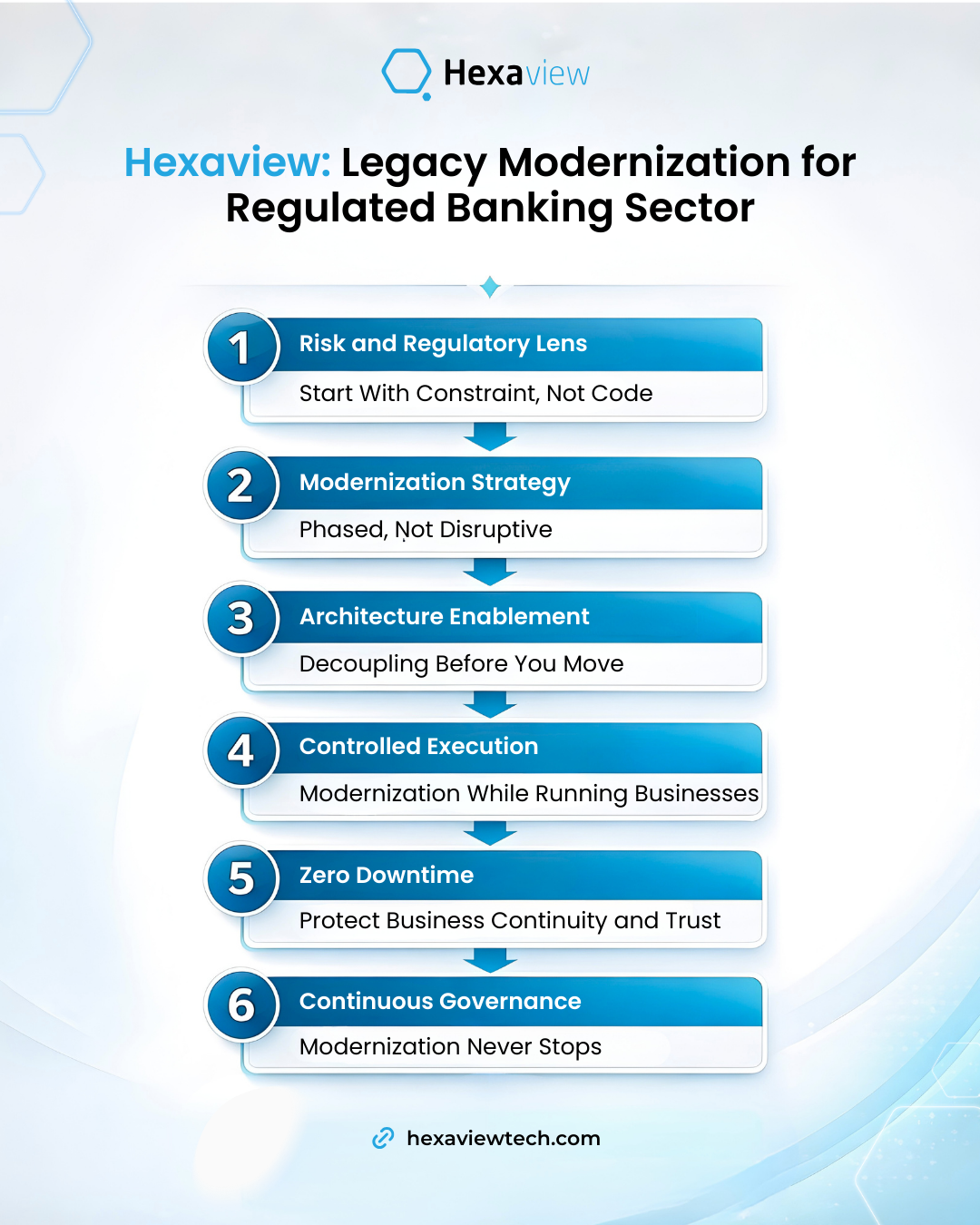

We start by understanding risk exposure, regulatory expectations, and data sensitivity. Modernization cannot start with technology choices when it comes to regulated sectors, but it starts with the following.

We do not replace everything at once but help to define a phased modernization roadmap. It generally includes the following.

This approach can reduce uncertainty and avoid the risk of large-scale disruption.

Before migrating systems, Hexaview mostly focuses on architectural decoupling.

It is a critical step that can successfully ensure banking system modernization and enable flexibility without affecting existing platforms.

Execution is performed in an incremental manner. We make use of.

When companies run legacy and modern systems parallel, it allows teams to validate performance, accuracy and compliance before processing further. This can dramatically reduce operational risk.

Cutovers are executed progressively, not abruptly. Hexaview ensures the following.

It is a disciplined approach to enable zero-downtime and preserve regulatory confidence and customer trust.

Modernization does not end after going live, but it is a continuous process.

It would ensure that modernization remains aligned with business requirements, evolving regulations, and growth strategies.

Banks that generally succeed in today’s modernization have some common traits. They treat modernization as a multi-year strategic program, not a short-term project. They are able to align business compliance, risk, and technology teams under the same vision. They can engage regulators early to build confidence and transparency.

One of the most important things is that they recognize legacy modernization in banking as a continued journey. It is something that requires ongoing investment, governance, and adaptability.

The strength of leadership of the banking sector in today’s environment is reflected in the resilience of the system. Institutions that delay modernization will only lose agility, accumulate risk and fall behind. Institutions that act decisively can build platforms that support growth, innovation, and compliance.

Legacy modernization in banking is no longer optional. This is a leadership responsibility that determines whether banks will operate securely, compete effectively, and comply confidently in today’s digital world.

1. Can banks modernize legacy systems without disrupting live operations?

Yes. It can be possible by phased modernization, progressive cutovers, and parallel system runs. This ensures legacy system modernization while keeping existing services live. This approach enables zero downtime and protects customer experience throughout the transformation.

2. How does legacy modernization support regulatory compliance?

Modernization improves data traceability, auditability, and reporting accuracy. By embedding compliance controls into architecture and migration processes, banks strengthen regulatory compliance while reducing manual effort and operational risk.

3. Is mainframe migration mandatory for legacy modernization in banking?

No. Mainframe migration is optional and should be strategic. Many banks modernize incrementally by decoupling systems first, modernizing selected workloads, and migrating only where it delivers clear risk or cost benefits.

.svg)

.svg)